In the ever-evolving digital landscape, the demand for custom loan app development in the UAE is rapidly increasing, especially in 2025. With the UAE’s financial sector embracing technological advancements, businesses are keen to provide digital loan apps that allow customers to apply for loans seamlessly from their mobile devices. But what does it take to build an instant loan app? The development costs can vary widely based on several factors, from the loan application features to the development team’s expertise.

In 2025, the Application Development Software market in the United Arab Emirates is projected to generate a revenue of US$531.57m, with a steady annual growth rate of 5.94%. By 2029, this figure is expected to reach US$669.56m, highlighting the UAE’s growing demand for digital solutions like custom loan app development. This growth is fueled by the country’s emphasis on digital transformation and innovation. While the United States is expected to dominate globally, with a projected US$97.64bn in 2025 revenue, the UAE is rapidly catching up.

For example, imagine a fintech startup looking to launch a personal loan app in the UAE. They need to integrate features such as loan calculators, chatbots for customer service, and secure document management. All of these elements influence the overall loan application development costs and as a fintech startup you must keep in mind various Strategies to cut loan application development costs. Whether you’re a business owner seeking to venture into the digital lending space or a decision-maker aiming to streamline your services, understanding the costs and Top features of a loan app involved will help you make informed decisions.

As we dive deeper into this guide, we will explore the strategies to cut loan application development costs, discuss the factors affecting the cost of loan app development, and break down the step-by-step process of building an instant loan app in the UAE. Additionally, we will provide the latest industry trends, such as how the UAE’s growing fintech sector is shaping the cost of building a loan app in UAE 2025.

Stay tuned as we unravel the essential aspects of loan application development, so you can start planning your app’s launch with confidence. At Webelight Solutions, we’ve helped businesses turn their digital dreams into reality by developing tailored loan apps that are both functional and cost-effective.

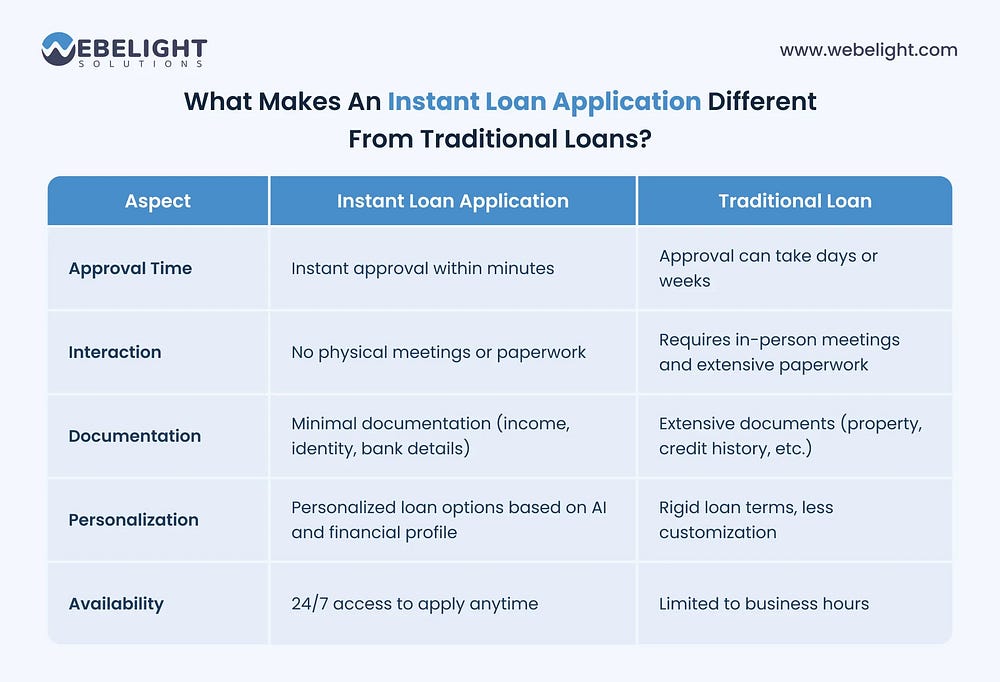

What Makes an Instant Loan Application Different from Traditional Loans?

Instant loan applications are transforming the way consumers access credit, providing an experience that is fundamentally different from traditional loans. Unlike conventional loans, which often require in-person visits, extensive paperwork, and prolonged approval processes, instant loan apps offer a quick, seamless borrowing experience entirely through mobile devices.

Here are the key differences:

1. Instant Approval and Disbursement

With an instant loan application, borrowers can receive loan approval within minutes, and the funds are typically disbursed into their account almost immediately. This stands in stark contrast to the traditional loan process, which can take several days or even weeks to complete. The speed of approval and instant disbursement make digital loans more appealing to consumers who need urgent financial assistance.

2. No Physical Interaction Required

Traditional loans often require multiple in-person meetings with bank representatives, along with lengthy paperwork. In contrast, digital loan apps allow users to apply for a loan, upload necessary documents, and receive approval all from their mobile devices. This contactless approach not only saves time but also enhances convenience.

3. Minimal Documentation

Instant loan applications often require less documentation than traditional loans. Borrowers typically only need to provide basic information such as their income, identity, and bank details. On the other hand, conventional loans might ask for property documents, credit histories, and other financial records. The simplified documentation process significantly lowers barriers for users who might not have access to traditional banking services.